It can be tricky to find the right insurance for an earthquake retrofit contractor, but we can help!

A general contractor recently called to ask if we can help with his insurance. He is a licensed earthquake retrofit contractor who has been working in construction for decades. He was struggling to find insurance that would actually cover his core operations: earthquake retrofit and foundation repair. When he met us, he had just purchased a policy that officially offered him no coverage for his main services.

Here was the message he had just received from his current broker:

Per our discussion, the policy that you purchased with us doesn’t cover foundation repair or earthquake retrofitting of any type. Unfortunately we must cancel your policy immediately. We will be unable to provide a replacement policy for you. We are sorry for the inconvenience.

At that moment the contractor had many retrofit jobs running simultaneously across the Bay Area, so this insurance problem had to be corrected immediately.

How did he find himself in this situation? The reason is because many brokers who work with contractors use instant-quoting portals that generate quick and cheap insurance quotes. These quotes are handy because of the speed and price, but they are usually riddled with exclusions. For a contractor who performs standard remodel work, these sorts of quotes might be the perfect fit. But for an earthquake retrofitter, the exclusions render these cheap quotes worthless.

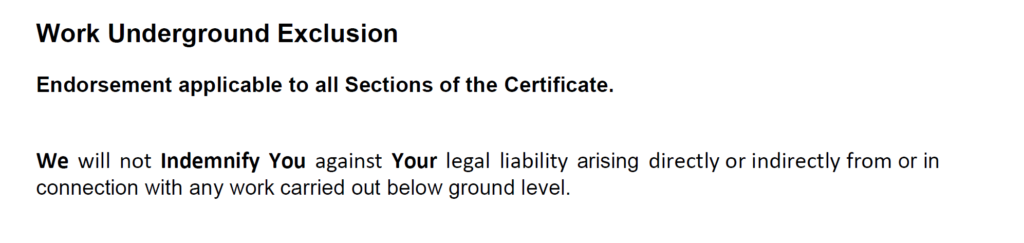

Here’s an example of such an exclusion:

Even though that exclusion for seismic retrofitting work seems pretty obvious, it’s still easy to miss it if the broker doesn’t read the quote carefully. Sometimes the exclusions are even more subtle, like this exclusion, which is often buried on page 80-something of the policy:

The contractor who called us had purchased a cheap policy that his broker had found for him instantly, via a portal that did not ask too many questions. The broker did not review the exclusions before starting the insurance, and carelessly sold a low-priced policy that contained an exclusion for all kinds of retrofitting work. A few weeks later, when the contractor was reviewing his new policy, he discovered the exclusion and called his broker. Only then did the broker realize that the insurance he had sold was worthless. The contractor realized, to his dismay, that he had been operating essentially uninsured for the past three weeks.

We were able to fix this problem for the earthquake retrofitter because we are experts at construction insurance of all kinds. We always read through the policy language before we put a new policy into force, and we know which exclusions to look for. We also know which insurers specialize in specific areas of construction which are often excluded on standard policies, such as earthquake retrofitting, bridge work, utility work, new construction, and remodel work performed for large HOAs. We made sure that the retrofitter got a liability policy that insured his actual operations and did not include any worrisome exclusions, so he could continue with his jobs uninterrupted.

If you are an earthquake retrofit contractor, or any kind of contractor who has struggled to find proper insurance, please reach out. We can help with general liability, workers comp, commercial auto, bonds, and any other kind of construction-related insurance.

Most importantly, we will make sure the job is done right the first time.

Many property owners are unaware of the fact that major construction is excluded from their standard insurance policy. This is true for homes, commercial buildings, and mixed use properties. If an owner wishes to renovate their property, changes must be made to the insurance policy, since the standard property policy most likely excludes any and all claims pertaining to a building under construction. In fact, many of these policies contain exclusions so strict that even if something unrelated to the construction damages the property during the remodel, it results in a denied claim. Let’s examine the following policy language from a standard homeowners insurance policy:

More likely than not, any loss would probably be at least indirectly related to the construction/renovation. In most cases it might be difficult to prove that a loss had NOTHING to do with renovation/construction, even if that is in fact the case. For example, if a kitchen fire breaks out in a building under construction, the presence of construction materials in the home may cause the fire to spread more rapidly an destroy the home. In this situation, the policy language above may be used to exclude coverage altogether, and thereby render the insurance policy worthless. During a period of construction, an owner must make sure to get a (temporary) insurance policy that is specifically designed to account for a building under construction.

So, what is the alternative? A Builders Risk (also referred to as a Course of Construction) policy is the answer. This is a type of packaged property and liability insurance policy that accounts for the risk posed by a construction project. Properties under construction often have higher risk for fires, theft/vandalism, water damage, and even risk of falling objects injuring people or property. A Builders Risk policy accounts for these risks. These policies also account for both the existing structure and the cost of the building materials on the property, whether on the premises or in transit.

Essentially, the way that a standard homeowners policy becomes a Builders Risk policy, is with the addition of an endorsement for Builders Risk coverage. Here’s an example of the language, clearly expanding coverage to construction:

For commercial buildings under construction, oftentimes a separate Builders Risk policy will temporarily replace the regular property policy, until construction is complete. Typically, these policies will last anywhere from 3-12 months, and are typically not renewed. Once construction is done, the Builders Risk policy is dropped, and the standard property policy is brought back again. For projects that take longer, such as new construction for larger buildings, longer policy terms are an option.

Many standard homeowners carriers do not offer Builders Risk policies. If this is the case with your carrier, we can help secure you a temporary Builders Risk policy to properly cover your home/building during construction. When construction is complete, we simply cancel the Builders Risk policy and refer you back to your previous insurer or we can make a referral to a trusted colleague.

What types of insurance does an interior designer need?

The main type of insurance an interior designer will need is Professional Liability (also known as Errors and Omissions). This is the insurance most likely to be required by the designer’s clients, whether the designer works directly with homeowners or as a contractor for a larger firm.

Professional Liability is basically “mistake insurance”. If the designer makes a costly professional error, this insurance steps in to foot the bill. This might mean a design error that delays a construction project, a mishap in ordering materials that doubles the cost of a project, or any other kind of on-the-job mistake. As long as the mistake was an honest professional error, this type of policy protects the designer from the large expenses (or court costs) that can come with fixing the mistake.

Ideally the policy language should make it clear that any professional error is covered. Here is an example of this kind of broad policy language:

We agree to pay on your behalf all sums which you become legally obliged to pay (including liability for claimants’ costs and expenses) as a result of any claim first made against you during the period of the policy arising out of your business activities for any negligent act, error, omission, misstatement or misrepresentation.

In other words, this policy will pay for any professional error the designer makes. It will pay for legal fees, court costs, and damages in the event the designer is sued for negligence, and will even cover the costs of a frivolous lawsuit. Ideally, the policy will say something like “We have a duty to defend any covered claim, even if such claim is groundless, false, or fraudulent.” This means that even if the carrier thinks a lawsuit is groundless, they are bound by their own contract language to defend the designer.

For designers who work as contractors for larger design/development firms, this type of insurance is almost certainly going to be a requirement prior to starting work. Firms that contract with independent designers want to make sure that if a mistake occurs, it isn’t going to bankrupt the designer (or become the responsibility of the firm). A policy with $1mil. limits is an affordable way for the designer to protect his/her own business, as well as the clients and firms he/she works with.

Many designers also have to visit jobs sites to meet with clients, architects, or general contractors. Therefore it may also be wise for the designer to add a General Liability policy as well.

General Liability insurance protects the designer in the event someone is injured at the job site and blames the designer. For example, while meeting with the client at the construction site, the client bumps his head and decides to sue the designer (who had set up the meeting). General Liability will foot the bill for claims related to bodily injury and property damage, whether the designer is actually to blame for the injury or not. For designers who meet with clientele at or near construction sites, a General Liability policy can be an crucial piece of protection.

When combined, these two policies shield the designer from most of the everyday risks associated with their work: they protect the designer from claims stemming from professional mistakes, design flaws, injuries on a job site, accidental damage to someone else’s property, and frivolous lawsuits.

What are some ways a designer can tell if their policy is high quality?

First, make sure the policy is part of an Architect’s and Engineers program. The front of the policy should look something like this:

This means that the policy takes into account the risks that come along with working in construction, even peripherally, and contains broad contract language and many industry-specific coverages. Long story short: this policy is more likely to pay a claim related to construction than a “miscellaneous” (a.k.a. boilerplate) Professional Liability policy.

Most importantly, an “Architects and Engineers” style policy will not contain the kinds of worrisome exclusions often found in “misc.” professional liability policies. It is crucial that the policy not contain clauses that exclude coverage for core parts of a designer’s business.

For example, say an interior design firm brought on an in-house engineer. Almost every “misc.” professional liability policy contains the following exclusion:

So all claims pertaining to engineering are automatically excluded from this policy. If the engineer makes a professional error, the legal fees and claim costs would NOT be covered! This is the danger of a “misc.” policy, rather than one tailored to a designer’s actual operation.

Construction-related lawsuits can take many forms. For example, a homeowner hires a general contractor who then sub-contracts in a number of electricians, plumbers, and other contractors. Meanwhile, the owner hires an interior designer to plan the interior. Ten years after the job is complete, the homeowner discovers a construction defect in the home, and decides to sue everyone that ever worked on the home in any capacity, including the interior designer. Even though the designer is not at fault and the job was a decade ago, he/she still has to pay for a lawyer, take time off work to appear in court, and pay travel expenses, just to make the claim go away. The interior designer’s insurance policies should cover all of these costs. Therefore the policy must contain language that encompasses even these sorts of peripheral construction lawsuits.

Imagine that designer had a “misc.” professional liability policy that contained the following typical exclusion: “This policy excludes all claims based upon, arising out of, directly or indirectly, or in any way involving suitability in design, or performance of any structure with respect to its ability to bear weight”. This policy language is designed to exclude coverage for just the type of lawsuit mentioned above. Though the designer had nothing to do with the defect, the carrier will use this language to deny the claim and refuse to pay the defense costs. In construction, lawsuits like this can pop up any time, so the policy must protect the designer from this common risk.

There are other ways to tell if an interior designer insurance policy is high quality:

Look for industry-specific extra coverages, such as coverage for Defense of Licensing Proceedings, FHA/OSHA/ADA regulatory proceedings, and automatic coverage for the designer’s sub-contractors.

A quality policy might contain Subpoena Assistance and Supplementary Payments, which covers the costs associated with taking off work or traveling to appear in court during a construction-related lawsuit.

Ideally, the policy should include something called “complimentary future claim mitigation”. This means that if the designer even suspects there may have been an error, or a dissatisfied (or overly litigious) client, the designer can contact the carrier before the situation turns into an actual claim. The carrier will advise the designer on how to address the situation and keep it from getting worse.

Another favorable coverage is Public Relations Crisis Management. In the event the designer needs to hire a public relations firm to repair the company’s reputation after a lawsuit or professional error, the carrier will pay for those costs as well.

In conclusion, an interior designer’s insurance needs are more intricate than meets the eye. There needs to be coverage for all kinds of construction-related lawsuits, and policy language that is tailored to fit the designer’s business.

If you would like to speak to a broker who has specialized in interior design insurance, reach out today to get a quote. They are also happy to review your current policy and explain what’s in it.

How to Insure a Damaged Building and/or a Building with Claims.

Is My Building Uninsurable??

It can be a frustrating experience to hear that your building is “uninsurable”. Oftentimes when a building has some unrepaired damage, a history of claims, or some other problem, many insurance professionals will simply shrug and say, “Sorry your building is probably uninsurable”. If you ever hear this, it usually means that that insurance professional actually doesn’t know how insure such a building. No building is uninsurable.

There are thousands of insurance companies in the US. For every possible type of property, there is an insurance company (or several) that specialize in insuring it. It is crucial to work with a knowledgeable broker who not only knows which carriers will insure damaged buildings, but also which coverage need to be added to the policy to fully protect you, the owner. This article will dive into how to properly insure a damaged building and/or a building with claims.

Insuring a Damaged Building

When a fire burns a portion of a home, or a burst pipe floods a couple floors of an apartment building, a common insurance scenario plays out. The owner files a claim with his/her insurance company, and that carrier pays the claim to cover the repairs. But then, upon renewal, the carrier cancels the policy and tells the owner to find insurance elsewhere. This can happen even while the building is still being repaired, or even before repairs have begun. The previous carrier may still be paying to repair the property, but meanwhile the building owner needs to seek new insurance for the now damaged property, in order to cover the property going forward.

Why does this happen? Insurance companies exist to make a profit, and when there is a claim they lose money. Insurance companies do not want to insure unprofitable clients. This is the basic rule that governs what an insurance company is willing to insure.

Simply put, when your insurance company starts losing money, your insurance coverage is in danger. It could be cancelled or non-renewed anytime at their request with only 30 days notice. This not only means that you need to shop for insurance again – it means that insurance has become much harder to find, because your building is damaged, and your claims history follows you.

Damaged buildings need insurance during the repair process. Vandalism, water damage, and fire damage are all real concerns while a building is being repaired. There are also other risks to consider when contractors and construction people are coming in and out of your building every day during the repair. Due to the increased risks of insuring a damaged building or a building under construction, many standard [sg_popup id=”907″ event=”click”]”admitted carriers”[/sg_popup] will likely decline to quote.

However there is a whole galaxy of options outside of the admitted market. These carriers specialize in insuring buildings that, for one reason or another, have been rejected (or priced out) of the admitted market. This includes damaged buildings, buildings with a history of claims, buildings under construction, and other unique situations.

Not every insurance professional knows how to access this portion of the insurance market. In fact, many insurance pros ONLY know how to shop the admitted market (or only have access to one single carrier); when those limited options offer only declines, that insurance pro waves the white flag. This can lead a building owner to (incorrectly) believe that their property needs to remain uninsured for the unforeseeable future.

Here at Mighty Oak, we know how to deal with these situations properly. We have relationships across the [sg_popup id=”907″ event=”click”]admitted AND the non-admitted markets[/sg_popup], so we are able to provide quotes to any property owner who needs insurance, even those with damaged buildings.

We also have the experience to know which coverage must be added to a damaged building’s insurance policy in order to fully protect the owner. For example, a policy for a building under construction should probably include a coverage such as [sg_popup id=”258″ event=”click”]Builder’s Risk[/sg_popup], while a policy for a vacant building needs to have the Vacant Property Exclusion removed prior to putting the policy in force. These (and other details) are what we look for when we help an owner of a damaged building acquire insurance.

What if your building isn’t damaged at all, but instead just has a long history of claims?

Earlier this year a homeowner contacted us with a predicament: her homeowner’s insurance had been cancelled after she filed one too many claims. Her house was in pristine condition, worth more than $2 million, yet it seemed like nobody could get her a homeowner’s insurance quote. Her claims history had made her “uninsurable” (or at least that’s what she feared).

For over ten years she had been with a standard carrier, just like all her neighbors. But one day a storm damaged her windows and caused a leak, so she filed a claim. The insurance company paid for the repairs. Soon after that, a tree fell on her fence – which meant another claim and another pay-out by the carrier. Finally a couple months after that, the neighbor’s landscape contractor backed over their lawn irrigation equipment and broke the sprinkler system. This claim cost the carrier another $5,000. Their insurance company canceled her policy about a month later, and their agent had no options to replace it.

When she visited another broker, he checked with all the standard, admitted carriers, and received nothing but declines. Why? Because with every carrier he checked, he was required to explain her claims history. When these carriers heard about the claims, they refused to take on the risk.

None of these these claims were catastrophic, and none were wildly expensive. All were reasonable claims that any insurance company should expect to pay for. Yet just the fact that there were three claims in one year was enough for the client to be shut out of the standard market, even though her house was in excellent condition. When her broker received nothing but declines, he told her she may be uninsurable.

Of course, he was wrong; she was very much insurable. When she was referred to us by a friend, we performed a diligent search of carriers that are willing to take on clients with a history of claims. We found her some quotes that fully insured her property, and she is now insured once more.

Our brokerage specializes in helping owners of “distressed” properties, whether that means buildings under construction, damaged building, or buildings with a history of claims. We can even find insurance for buildings where damage has yet to be repaired. There is a carrier for every situation; no client is uninsurable. We will put our deep knowledge of the insurance market to work for any client that needs insurance, especially those who have been turned away by other brokers.