It can be tricky to find the right insurance for an earthquake retrofit contractor, but we can help!

A general contractor recently called to ask if we can help with his insurance. He is a licensed earthquake retrofit contractor who has been working in construction for decades. He was struggling to find insurance that would actually cover his core operations: earthquake retrofit and foundation repair. When he met us, he had just purchased a policy that officially offered him no coverage for his main services.

Here was the message he had just received from his current broker:

Per our discussion, the policy that you purchased with us doesn’t cover foundation repair or earthquake retrofitting of any type. Unfortunately we must cancel your policy immediately. We will be unable to provide a replacement policy for you. We are sorry for the inconvenience.

At that moment the contractor had many retrofit jobs running simultaneously across the Bay Area, so this insurance problem had to be corrected immediately.

How did he find himself in this situation? The reason is because many brokers who work with contractors use instant-quoting portals that generate quick and cheap insurance quotes. These quotes are handy because of the speed and price, but they are usually riddled with exclusions. For a contractor who performs standard remodel work, these sorts of quotes might be the perfect fit. But for an earthquake retrofitter, the exclusions render these cheap quotes worthless.

Here’s an example of such an exclusion:

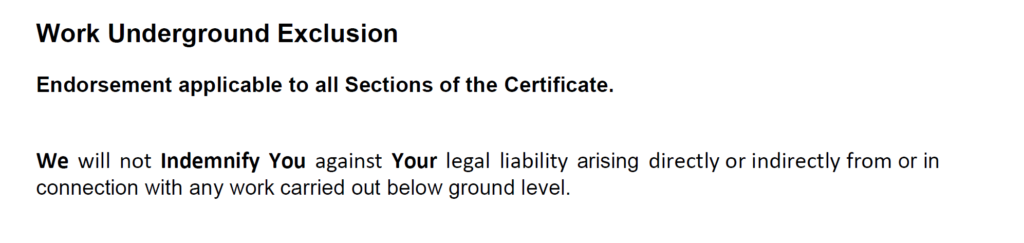

Even though that exclusion for seismic retrofitting work seems pretty obvious, it’s still easy to miss it if the broker doesn’t read the quote carefully. Sometimes the exclusions are even more subtle, like this exclusion, which is often buried on page 80-something of the policy:

The contractor who called us had purchased a cheap policy that his broker had found for him instantly, via a portal that did not ask too many questions. The broker did not review the exclusions before starting the insurance, and carelessly sold a low-priced policy that contained an exclusion for all kinds of retrofitting work. A few weeks later, when the contractor was reviewing his new policy, he discovered the exclusion and called his broker. Only then did the broker realize that the insurance he had sold was worthless. The contractor realized, to his dismay, that he had been operating essentially uninsured for the past three weeks.

We were able to fix this problem for the earthquake retrofitter because we are experts at construction insurance of all kinds. We always read through the policy language before we put a new policy into force, and we know which exclusions to look for. We also know which insurers specialize in specific areas of construction which are often excluded on standard policies, such as earthquake retrofitting, bridge work, utility work, new construction, and remodel work performed for large HOAs. We made sure that the retrofitter got a liability policy that insured his actual operations and did not include any worrisome exclusions, so he could continue with his jobs uninterrupted.

If you are an earthquake retrofit contractor, or any kind of contractor who has struggled to find proper insurance, please reach out. We can help with general liability, workers comp, commercial auto, bonds, and any other kind of construction-related insurance.

Most importantly, we will make sure the job is done right the first time.