It can be tricky to find the right insurance for an earthquake retrofit contractor, but we can help!

A general contractor recently called to ask if we can help with his insurance. He is a licensed earthquake retrofit contractor who has been working in construction for decades. He was struggling to find insurance that would actually cover his core operations: earthquake retrofit and foundation repair. When he met us, he had just purchased a policy that officially offered him no coverage for his main services.

Here was the message he had just received from his current broker:

Per our discussion, the policy that you purchased with us doesn’t cover foundation repair or earthquake retrofitting of any type. Unfortunately we must cancel your policy immediately. We will be unable to provide a replacement policy for you. We are sorry for the inconvenience.

At that moment the contractor had many retrofit jobs running simultaneously across the Bay Area, so this insurance problem had to be corrected immediately.

How did he find himself in this situation? The reason is because many brokers who work with contractors use instant-quoting portals that generate quick and cheap insurance quotes. These quotes are handy because of the speed and price, but they are usually riddled with exclusions. For a contractor who performs standard remodel work, these sorts of quotes might be the perfect fit. But for an earthquake retrofitter, the exclusions render these cheap quotes worthless.

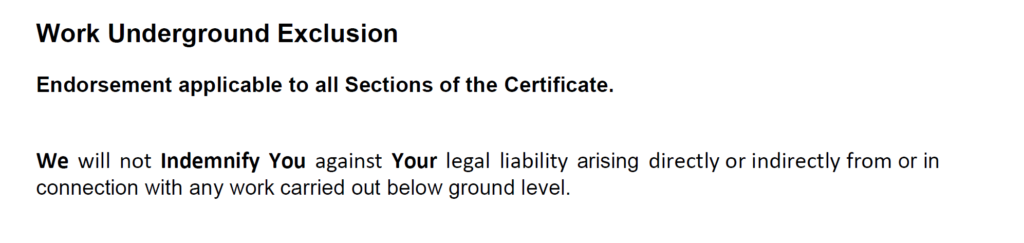

Here’s an example of such an exclusion:

Even though that exclusion for seismic retrofitting work seems pretty obvious, it’s still easy to miss it if the broker doesn’t read the quote carefully. Sometimes the exclusions are even more subtle, like this exclusion, which is often buried on page 80-something of the policy:

The contractor who called us had purchased a cheap policy that his broker had found for him instantly, via a portal that did not ask too many questions. The broker did not review the exclusions before starting the insurance, and carelessly sold a low-priced policy that contained an exclusion for all kinds of retrofitting work. A few weeks later, when the contractor was reviewing his new policy, he discovered the exclusion and called his broker. Only then did the broker realize that the insurance he had sold was worthless. The contractor realized, to his dismay, that he had been operating essentially uninsured for the past three weeks.

We were able to fix this problem for the earthquake retrofitter because we are experts at construction insurance of all kinds. We always read through the policy language before we put a new policy into force, and we know which exclusions to look for. We also know which insurers specialize in specific areas of construction which are often excluded on standard policies, such as earthquake retrofitting, bridge work, utility work, new construction, and remodel work performed for large HOAs. We made sure that the retrofitter got a liability policy that insured his actual operations and did not include any worrisome exclusions, so he could continue with his jobs uninterrupted.

If you are an earthquake retrofit contractor, or any kind of contractor who has struggled to find proper insurance, please reach out. We can help with general liability, workers comp, commercial auto, bonds, and any other kind of construction-related insurance.

Most importantly, we will make sure the job is done right the first time.

A mixed use apartment building in Chinatown, San Francisco

What is a “mixed use” property?

A building is “mixed-use” if it has businesses on the street level and apartments up above. Really, a mixed use building is any building that serves multiple functions. It might be part office and part retail, or part government building and part cafe, or part residential and part commercial. Walk around any major city – such as San Francisco – and you’ll see these types of buildings everywhere, especially mixed use apartments. Here at Mighty Oak, we specialize in mixed use property insurance.

Another mixed use apartment building in Chinatown, San Francisco

The Challenge of Insuring Such a Building

Mixed use apartments, which generally feature apartments on top and businesses on the street level, are ubiquitous in San Francisco. They also happen to be a real pickle to insure properly. Every occupant of this building needs a different kind of insurance: the business owner needs to insure his business, the residential tenant needs to insure his belongings, and the building owner needs to insure the entire property.

In the event of a disaster like a fire, it is crucial that all three of those areas (business, tenant’s belongings, and the building itself) have policies that will pay out! Often times the business owners, tenants, and landlords aren’t entirely clear on which types of insurance they actually need, or what it means to be “properly covered”. For example, if a building owner insures his building, it is important for the business owner tenant to understand that his business property is likely NOT covered at all.

Often these buildings contain many different tenants and businesses that each have their own unique insurance needs. It is absolutely essential to work with a competent insurance broker who can provide insurance options for the business owners, the tenants, and the landlord. Ideally this broker could also educate the whole crew on which occupants are responsible for which insurance pieces.

This iconic corner in North Beach, San Francisco is full of mixed use apartment buildings.

How to Properly Insure a Mixed Use Building

First, we should consider the building itself. Each building needs to have its own Landlords Policy, which will cover the actual building. As the name of the policy implies, this piece is the landlord’s obligation to purchase (and it is the landlord who gains the protection). If the building is damaged or destroyed, this policy will pay back the owner of the property for repairs. Sometimes when an older building is damaged, the city steps in and demands that the property be brought up to code (such as a mandatory earthquake retrofit). This insurance policy can help cover that cost as well. It will even cover lost income, since the owner may lose some rent payments if tenants have to evacuate during repairs.

This policy is crucial for the owner in other ways. For example, if a visitor slips in the stairwell and decides to sue the property owner, this policy will pay the legal bills and damages. If a tenant decides he’s been wrongfully evicted and chooses to sue, this policy may cover the landlord’s legal fees. In other words, the building is the landlord’s business, so it should be insured in almost all the same ways a business would be insured: protect the property itself, protect the owner’s income, and protect the owner from lawsuits.

A typical mixed use property, with apartments upstairs and a bar downstairs. The owner must insure this entire property, since he owns the whole building.

Now that the building itself is covered, the rest of the building’s inhabitants (both residential tenants and business owners) need their own separate insurance. Take the example below: we see that the red units are residential units and the blue units are retail commercial units.

Each occupied unit needs its own insurance coverage. But wait – haven’t we already insured the building? Why should each tenant have to insure their own unit? Actually the tenants do not need to insure any part of the building itself, but rather their own belongings inside their unit. The Landlord’s Policy will not cover any of the tenant’s belongings, and in the event of a fire, the tenant will not be reimbursed for lost items unless he carries his own separate Renter’s Policy.

A Renter’s Policy is also known as “contents coverage”, or insurance coverage that does not cover the structure itself, but instead the contents of each unit. Every residential tenant can cover his own belongings without having to pay for coverage for the building that he does not own. These policies are designed to protect the tenant in case something like a burst pipe destroys their belongings. A good Renter’s Policy can even cover a tenant’s liability, say if the tenant accidentally starts a fire that destroys the neighboring tenant’s belongings. The combo of a Landlord’s Policy and Renter’s Policy ensures that the building itself and all the stuff inside it are protected from accident or disaster.

What about the businesses on the ground floor? They are also tenants, but they don’t live in their unit. These commercial tenants need policies that cover their:

Business Property – Covers their equipment, tools, and other contents of the commercial unit, in case they need to be replaced after an accident or disaster.

General Liability– Covers the business owner in case a customer gets injured or someone else’s property is damaged during the normal course of business. If someone slips inside the business and decides to sue the business owner, this policy will pay his legal bills.

Workers Comp– If an employee is injured on the job, this policy will pay the medical bills. This type of insurance is legally required for any business that has at least one employee.

Just like the residential tenants, these business owners do not need to cover any part of the building itself, but only their own businesses inside their unit

This is why a mixed use property is the perfect intersection of personal insurance and commercial insurance, all in one property. A good broker can work with the entire building to cover the owner and every tenant in a way that protects everyone without forcing anyone to pay for insurance they don’t need.

A professional handyman has to be pretty adaptable! Installing a set of cabinets, repairing some drywall, painting a mailbox, realigning a garage door, pouring some concrete, sanding a porch, assembling furniture, removing a door frame, building a shelving unit, remodeling a living room, unclogging a drain, hauling some junk… it’s all part of the job. The more skills a handyman can master, the more jobs he can say yes to.

A handyman’s business insurance needs to be just as adaptable. The more jobs a handyman can take on, the more varied the risks that come with those jobs, and the handyman’s policies MUST cover all those risks in order to be effective (otherwise what’s the point of insurance?). Therefore it is crucially important that the handyman work closely with a business insurance broker to craft an insurance policy that is tailored to the handyman’s actual needs. Being “properly covered” doesn’t mean just piling on more and more insurance (with higher commissions for the broker); it means creating a set of policies that fit a client’s business risks exactly.

“Do I really need insurance?”

The first question many handymen (and other business owners) ask is, “Do I really need insurance?” A good way to answer that question is to think about the risks a handyman takes on just by doing his job, AKA the every day accidents that could result in the handyman having to shell out lots and lots (and lots) of money. A newly installed air conditioning unit could fall and injure a child. A handyman’s assistant could slip off a ladder and break his leg. The handyman could get T-boned while driving his truck to a job site. A client could trip over a peeled-up carpet and decide to sue. A whole set of new tools could be stolen from the truck. And many many more.

These sorts of accidents can happen to anybody, even the most skilled operators. They are the risks of doing business. What insurance does is transfer that risk off of the handyman’s balance sheet and onto the balance sheet of an insurance company. One single lawsuit or car accident can put even a well-established handyman out of business. One theft can set a handyman back for months. By purchasing policies designed to cover these mishaps, the handyman can sleep at night with the knowledge that no matter what goes wrong, he won’t have to pay for the damage. That is, as long as the risk is covered in the policy.

This is why it’s so crucial to work with an insurance broker who isn’t just trying to close a deal quickly for a fast buck, but instead wants to learn every facet of the handyman’s business before agreeing to write the insurance policies. The cost and scope of the insurance will depend on what kind of work the handyman does, whether he has employees, who his clients are, and how large his operation is. If the handyman does more dangerous work, the cost will be higher, but so will the coverage. All of this should be discussed before the broker even attempts to get quotes.

One added perk of insurance: Many clients require certificates of insurance before work can begin. These clients may include apartment complexes, bank-owned properties, clients asking for electrical or plumbing work, and clients who simply want to ensure that if an accident does occur on their property, the handyman will have the resources to pay for the repairs. For these clients, a handyman without insurance is simply unhireable. Therefore proper insurance coverage could lead to more (and better paying) jobs.

Remember: Even if you are very careful and diligent at job sites, accidents can still happen. Insurance protects you and your business from outcomes that are out of your control.

“What types of insurance do I need?”

The types of insurance a handyman might typically need include:

[sg_popup id=”246″ event=”click”]General Liability[/sg_popup] – Protects him from paying repair costs in the event that the handyman accidentally harms a customer’s home, appliances, or other property. If the customer himself is injured in an accident, this insurance can cover small medical bills regardless of who was at fault, and large medical bills if the handyman is found to be liable. Should the accident lead to a pricey lawsuit, this policy could cover all the defense costs. A General Liability policy can even pay out if there is a dispute over the handyman’s finished work – this is known as “Completed Products Coverage”. Since so much of his work is performed within a customer’s home, a professional handyman must have protection from lawsuits of all varieties. A G.L. policy provides just that, so a handyman can do his job without worrying that one mistake will cost him his business.

Coverage of tools and equipment (also known as [sg_popup id=”557″ event=”click”]Inland Marine[/sg_popup]) – If his tools or equipment are stolen, damaged, or lost, this policy will cover the loss. Imagine the cost to replace an entire set of tools if they are destroyed by fire or some other accident. Inland Marine will not only pay to replace the set, but it may also cover lost income if the accident forced the handyman to suspend his operations for a time. And to top it all off, Inland Marine coverage follows the handyman wherever he takes his equipment (unlike a [sg_popup id=”256″ event=”click”]Commercial Property[/sg_popup] policy, which covers only equipment and property that stays in one place). Since most handymen do a lot of traveling with their tools, every piece of a handyman’s equipment should be insured with an Inland Marine policy.

[sg_popup id=”249″ event=”click”]Workers Comp[/sg_popup] – If the handyman has employees, this insurance is legally required. It covers medical bills, lost wages, and even death benefits if employees are injured or killed on the job. The more dangerous the work, the more expensive this policy is likely to be. But don’t take that to mean it’s a policy that can be skipped. Aside from the legal requirement, Workers Comp is an absolutely crucial policy for a handyman to carry, just for the sake of his business. Given the strenuous, physical nature of the work, the threat of accidental injury is always present. Workers Comp will not only cover the medical bills for the employees (and the owner if he wants to be included), but it also protects the owner from lawsuits.

[sg_popup id=”251″ event=”click”]Commercial Auto[/sg_popup] – Since being a professional handyman involves the daily operation of a work vehicle, having a strong Commercial Auto policy in place is vital. Whether driving to a job site, picking up supplies, backing into a customer’s driveway, or popping out for coffee, every moment spent on the road exposes a handyman to risk. Without a Commercial Auto policy in place, the handyman is on the hook for any harm that comes to people or property as a result of his vehicle (whether the business owner or his employees are driving). If a handyman’s truck backs into some scaffolding, gets T-boned at an intersection, rear-ends a car in traffic, or strikes a pedestrian, this crucial coverage can pay for the damages. It can cover medical bills, replacement of damages property, legal fees, and even repairs to the handyman’s own vehicle should he be hit by an uninsured driver.

The Shield

These policies combine to form a shield that protects a handyman from just about any catastrophe that could strike his business: injured workers, a car accident, a fire at the shop, theft of tools, damage to a customer’s property, a natural disaster, and even lawsuits from dissatisfied customers. This is what we call a “well-tailored” policy, rather than “one size fits all”. It doesn’t just tack on a bunch of insurance a handyman doesn’t actually need; instead it is designed specifically for a handyman, and covers exactly the risks he might face.

To compile such a perfectly tailored policy, it’s usually best to work with a business insurance broker, because brokers can search the whole market for the best deal. Brokers have access to insurance carriers that specialize in handymen and tradesmen of all kinds.

Want to find the right insurance for your business? Drop us a line! You can speak to broker, ask a question, or even suggest a future blog post.